Australia’s corporate sustainability landscape is undergoing a major transformation. From January 2025, the Australian Sustainability Reporting Standards (ASRS) became mandatory for large businesses, requiring them to disclose not only their emissions but also the financial risks and opportunities associated with climate change.

ASRS is more than just an extension of the National Greenhouse and Energy Reporting (NGER) scheme. It introduces a new level of rigour and accountability, including external audits and director liability for inaccurate disclosures. The standards require climate-related financial disclosures, scenario analysis, and a detailed climate transition plan covering Scope 1, 2, and 3 emissions. This shift elevates sustainability reporting to a strategic, board-level concern.

ASRS draws heavily from voluntary frameworks such as CDP, GRI, and the Science Based Targets initiative (SBTi). Many companies already reporting under these standards—particularly in property management and manufacturing—are well-positioned to transition. However, sectors like government, healthcare, and education face a steeper learning curve, having had limited exposure to structured climate reporting.

But organisations that treat ASRS as a compliance exercise risk missing the bigger picture. Reporting is not the end goal—it’s a tool to inform and accelerate decarbonisation. The most forward-thinking organisations are already aligning their reporting with operational strategies, using emissions data to identify inefficiencies, prioritise investments, and engage stakeholders across the value chain. This integrated approach not only ensures compliance but also builds resilience and competitive advantage.

Who reports what and when: ASRS rollout timeline

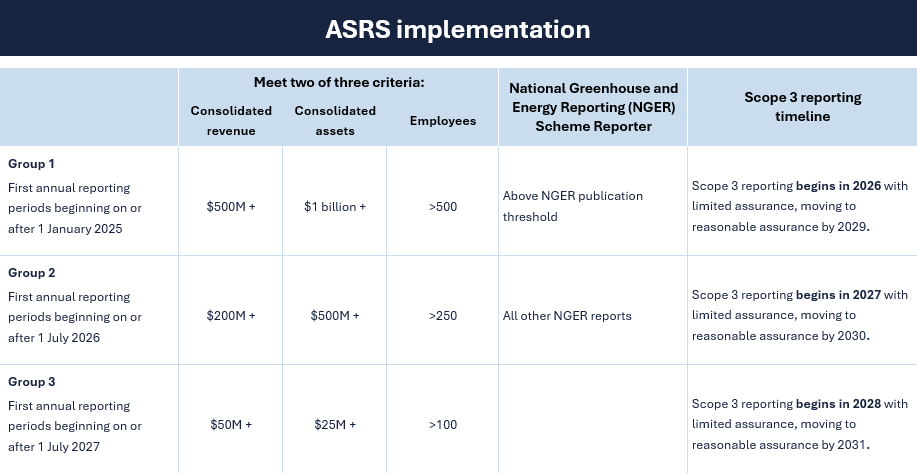

The rollout of ASRS is being implemented in three tranches, based on company size and financial thresholds. Each group will also follow a phased approach to Scope 3 reporting, with a three-year transition period from limited to reasonable assurance:

The information in the above table is based on publicly available guidance from the Australian Sustainability Reporting Standards (ASRS), as issued by the Australian Accounting Standards Board (AASB). This summary is provided for informational purposes only and does not constitute official regulatory advice.

While Group 3 reporters have more time, they are not insulated from early action. Many Group 1 companies—especially in retail, food, and manufacturing—are already requesting Scope 3 data from their suppliers. This means that smaller businesses in the supply chain may face indirect reporting obligations well before their formal ASRS start date. Early preparation is key to staying ahead of these expectations.

Eight tips for embedding Australian Sustainability Reporting Standards into your decarbonisation strategy

As organisations navigate ASRS, several cross-sector lessons have emerged that can guide a more integrated and effective approach to climate reporting and decarbonisation:

Start with Scope 2 for immediate impact

Decarbonising Scope 2 emissions—typically through renewable electricity procurement and energy efficiency—offers a relatively accessible starting point. Market-based mechanisms such as power purchase agreements (PPAs), renewable energy certificates, and on-site solar installations can deliver measurable reductions while aligning with ASRS reporting requirements.

Optimise energy use before offsetting

With renewable energy often carrying a cost premium, improving energy efficiency is a critical first step. Reducing overall consumption not only lowers emissions but also enhances the cost-effectiveness of any renewable energy strategy.

Take a phased approach to Scope 1 decarbonisation

Scope 1 emissions, often tied to fuel combustion or industrial processes, can be more complex to address. A progressive strategy—starting with energy audits, followed by electrification or fuel switching—allows organisations to balance decarbonisation goals with operational and financial realities.

Engage the value chain early for Scope 3

While ASRS allows a three-year transition period for Scope 3 reporting to move from limited to reasonable assurance, the pressure to act is already mounting. Major retailers like Coles and Woolworths are pushing voluntary Scope 3 disclosures down their supply chains, particularly in food, beverage, and agriculture. This means that even non-Tranche 1 reporters will soon face indirect reporting obligations.

Scope 3 emissions are notoriously difficult to quantify, often involving complex supply chains and data gaps. However, early engagement with suppliers and value-chain partners can significantly improve data quality and reduce the burden of future compliance. Companies that start building their Scope 3 inventories now will be better prepared for the inevitable expansion of mandatory reporting.

Use reporting to drive strategy, not just compliance

Climate reporting should not be treated as a standalone task. Instead, it should be embedded into broader business planning, risk management, and capital allocation processes. This ensures that disclosures are not only accurate but also actionable.

Leverage existing frameworks to accelerate readiness

Many organisations already reporting under voluntary frameworks like CDP, GRI, or SBTi can use these as a foundation for ASRS compliance. Conducting a gap analysis between current practices and ASRS requirements can streamline the transition and highlight areas for improvement.

Build internal capability and governance

Successful implementation of ASRS requires more than technical expertise—it demands strong governance, cross-functional collaboration, and board-level oversight. Investing in internal capability and stakeholder education will be key to sustaining long-term compliance and performance.

Materiality and scenario planning are critical

Understanding which climate risks and opportunities are most material to your business—and how they may evolve under different climate scenarios—is essential. This insight informs both the disclosures required under ASRS and the strategic decisions that follow.

Australian Sustainability Reporting Standards: From reporting to resilience

ASRS is no longer on the horizon—it’s here. The organisations that will thrive under this new regime are those that treat reporting not as a checkbox, but as a catalyst for transformation. By embedding climate risk into financial planning, engaging the value chain, and prioritising energy data management, businesses can turn compliance into a competitive edge.

The focus now should be on building internal capability, educating stakeholders, and strengthening governance. The transition is already underway—those who act decisively will not only meet their obligations but lead the way in building a resilient, low-carbon future.

Contact us for more information

To learn more about how World Kinect experts can support your business, click below: